Time Series Analysis 1¶

In the first lecture, we are mainly concerned with how to manipulate and smooth time series data.

In [1]:

%matplotlib inline

import matplotlib.pyplot as plt

In [2]:

import os

import time

In [3]:

import numpy as np

import pandas as pd

In [4]:

import gmaps

import gmaps.datasets

Dates and times¶

Timestamps¶

In [5]:

now = pd.to_datetime('now')

In [6]:

now

Out[6]:

Timestamp('2018-11-04 17:15:19.437536')

In [7]:

now.year, now.month, now.week, now.day, now.hour, now.minute, now.second, now.microsecond

Out[7]:

(2018, 11, 44, 4, 17, 15, 19, 437536)

In [8]:

now.month_name(), now.day_name()

Out[8]:

('November', 'Sunday')

Formatting timestamps¶

See format codes

In [9]:

now.strftime('%I:%m%p %d-%b-%Y')

Out[9]:

'05:11PM 04-Nov-2018'

Parsing time strings¶

pandas can handle standard formats¶

In [10]:

ts = pd.to_datetime('6-Dec-2018 4:45 PM')

In [11]:

ts

Out[11]:

Timestamp('2018-12-06 16:45:00')

For unusual formats, use strptime¶

In [12]:

ts = pd.datetime.strptime('10:11PM 02-Nov-2018', '%I:%m%p %d-%b-%Y')

In [13]:

ts

Out[13]:

datetime.datetime(2018, 11, 2, 22, 0)

Intervals¶

In [14]:

then = pd.to_datetime('now')

time.sleep(5)

now = pd.to_datetime('now')

In [15]:

now - then

Out[15]:

Timedelta('0 days 00:00:05.004077')

Date ranges¶

A date range is just a collection of time stamps.

In [16]:

dates = pd.date_range(then, now, freq='s')

In [17]:

dates

Out[17]:

DatetimeIndex(['2018-11-04 17:15:19.500621', '2018-11-04 17:15:20.500621',

'2018-11-04 17:15:21.500621', '2018-11-04 17:15:22.500621',

'2018-11-04 17:15:23.500621', '2018-11-04 17:15:24.500621'],

dtype='datetime64[ns]', freq='S')

In [18]:

(then - pd.to_timedelta('1.5s')) in dates

Out[18]:

False

Periods¶

Periods are intervals, not a collection of timestamps.

In [19]:

span = dates.to_period()

In [20]:

span

Out[20]:

PeriodIndex(['2018-11-04 17:15:19', '2018-11-04 17:15:20',

'2018-11-04 17:15:21', '2018-11-04 17:15:22',

'2018-11-04 17:15:23', '2018-11-04 17:15:24'],

dtype='period[S]', freq='S')

In [21]:

(then + pd.to_timedelta('1.5s')) in span

Out[21]:

True

Lag and lead with shift¶

We will use a periodic time series as an example. Periodicity is important because many biological phenomena are linked to natural periods (seasons, diurnal, menstrual cycle) or are intrinsically periodic (e.g. EEG, EKG measurements).

In [22]:

index = pd.date_range('1-1-2018', '31-1-2018', freq='12h')

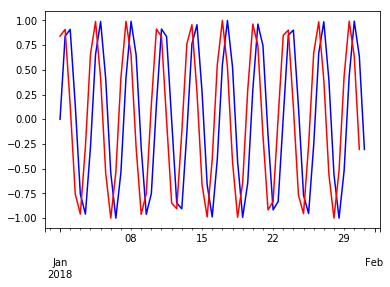

You can shift by periods or by frequency. Shifting by frequency maintains boundary data.

In [23]:

wave = pd.Series(np.sin(np.arange(len(index))), index=index)

In [24]:

wave.shift(periods=1).head(3)

Out[24]:

2018-01-01 00:00:00 NaN

2018-01-01 12:00:00 0.000000

2018-01-02 00:00:00 0.841471

Freq: 12H, dtype: float64

In [25]:

wave.shift(periods=1).tail(3)

Out[25]:

2018-01-30 00:00:00 0.436165

2018-01-30 12:00:00 0.992873

2018-01-31 00:00:00 0.636738

Freq: 12H, dtype: float64

In [26]:

wave.shift(freq=1).head(3)

Out[26]:

2018-01-01 12:00:00 0.000000

2018-01-02 00:00:00 0.841471

2018-01-02 12:00:00 0.909297

Freq: 12H, dtype: float64

In [27]:

wave.shift(freq=1).tail(3)

Out[27]:

2018-01-30 12:00:00 0.992873

2018-01-31 00:00:00 0.636738

2018-01-31 12:00:00 -0.304811

Freq: 12H, dtype: float64

In [28]:

wave.plot()

pass

In [29]:

wave.plot(c='blue')

wave.shift(-1).plot(c='red')

pass

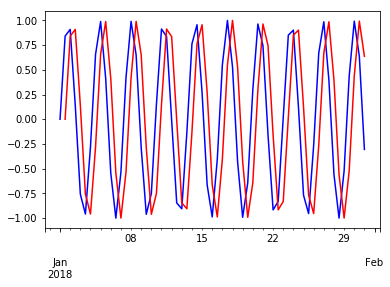

In [30]:

wave.plot(c='blue')

wave.shift(1).plot(c='red')

pass

In [31]:

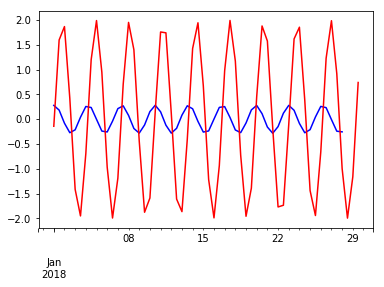

(wave - wave.shift(-6)).plot(c='blue')

(wave - wave.shift(-3)).plot(c='red')

pass

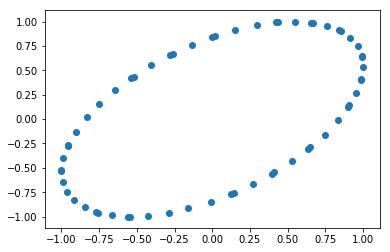

Embedding the time series with its lagged version reveals its periodic nature.

In [32]:

plt.scatter(wave, wave.shift(-1))

pass

Find percent change from previous period¶

In [33]:

wave.pct_change().head()

Out[33]:

2018-01-01 00:00:00 NaN

2018-01-01 12:00:00 inf

2018-01-02 00:00:00 0.080605

2018-01-02 12:00:00 -0.844803

2018-01-03 00:00:00 -6.362829

Freq: 12H, dtype: float64

pct_change is just a convenience wrapper around the use of shift

In [34]:

((wave - wave.shift(-1, freq='12h'))/wave).head()

Out[34]:

2017-12-31 12:00:00 NaN

2018-01-01 00:00:00 -inf

2018-01-01 12:00:00 -0.080605

2018-01-02 00:00:00 0.844803

2018-01-02 12:00:00 6.362829

Freq: 12H, dtype: float64

Resampling and window functions¶

The resample and window method have the same syntax as groupby,

in that you can apply an aggregate function to the new intervals.

Resampling¶

Sometimes there is a need to generate new time intervals, for example, to regularize irregularly timed observations.

Down-sampling¶

In [35]:

index = pd.date_range(pd.to_datetime('1-1-2018'), periods=365, freq='d')

In [36]:

series = pd.Series(np.arange(len(index)), index=index)

In [37]:

series.head()

Out[37]:

2018-01-01 0

2018-01-02 1

2018-01-03 2

2018-01-04 3

2018-01-05 4

Freq: D, dtype: int64

In [38]:

sereis_weekly_average = series.resample('w').mean()

sereis_weekly_average.head()

Out[38]:

2018-01-07 3

2018-01-14 10

2018-01-21 17

2018-01-28 24

2018-02-04 31

Freq: W-SUN, dtype: int64

In [39]:

sereis_monthly_sum = series.resample('m').sum()

sereis_monthly_sum.head()

Out[39]:

2018-01-31 465

2018-02-28 1246

2018-03-31 2294

2018-04-30 3135

2018-05-31 4185

Freq: M, dtype: int64

In [40]:

sereis_10day_median = series.resample('10d').median()

sereis_10day_median.head()

Out[40]:

2018-01-01 4.5

2018-01-11 14.5

2018-01-21 24.5

2018-01-31 34.5

2018-02-10 44.5

dtype: float64

Up-sampling¶

For up-sampling, we need to figure out what we want to do with the missing values. The usual choices are forward fill, backward fill, or interpolation using one of many built-in methods.

In [41]:

upsampled = series.resample('12h')

In [42]:

upsampled.asfreq()[:5]

Out[42]:

2018-01-01 00:00:00 0.0

2018-01-01 12:00:00 NaN

2018-01-02 00:00:00 1.0

2018-01-02 12:00:00 NaN

2018-01-03 00:00:00 2.0

Freq: 12H, dtype: float64

In [43]:

upsampled.ffill().head()

Out[43]:

2018-01-01 00:00:00 0

2018-01-01 12:00:00 0

2018-01-02 00:00:00 1

2018-01-02 12:00:00 1

2018-01-03 00:00:00 2

Freq: 12H, dtype: int64

In [44]:

upsampled.bfill().head()

Out[44]:

2018-01-01 00:00:00 0

2018-01-01 12:00:00 1

2018-01-02 00:00:00 1

2018-01-02 12:00:00 2

2018-01-03 00:00:00 2

Freq: 12H, dtype: int64

In [45]:

upsampled.interpolate('linear').head()

Out[45]:

2018-01-01 00:00:00 0.0

2018-01-01 12:00:00 0.5

2018-01-02 00:00:00 1.0

2018-01-02 12:00:00 1.5

2018-01-03 00:00:00 2.0

Freq: 12H, dtype: float64

Window functions¶

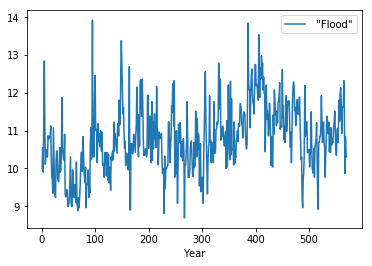

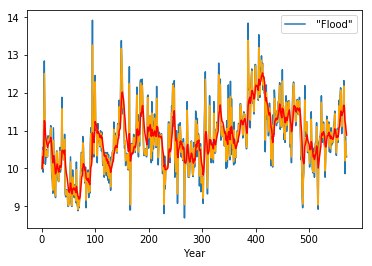

Window functions are typically used to smooth time series data. There are 3 variants - rolling, expanding and exponentially weighted. We use the Nile flooding data for these examples.

In [46]:

df = pd.read_csv('data/nile.csv', index_col=0)

In [47]:

df.head()

Out[47]:

| "Flood" | |

|---|---|

| Year | |

| 1 | 9.9974 |

| 2 | 10.5556 |

| 3 | 9.9014 |

| 4 | 11.4800 |

| 5 | 12.8460 |

In [48]:

df.plot()

pass

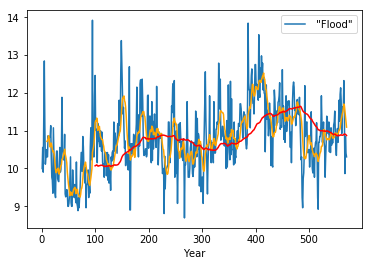

Rolling windows generate windows of a specified width¶

In [49]:

ts = pd.DataFrame(dict(ts=np.arange(5)))

ts['rolling'] = ts.rolling(window=3).sum()

ts

Out[49]:

| ts | rolling | |

|---|---|---|

| 0 | 0 | NaN |

| 1 | 1 | NaN |

| 2 | 2 | 3.0 |

| 3 | 3 | 6.0 |

| 4 | 4 | 9.0 |

In [50]:

rolling10 = df.rolling(window=10)

rolling100 = df.rolling(window=100)

In [51]:

df.plot()

plt.plot(rolling10.mean(), c='orange')

plt.plot(rolling100.mean(), c='red')

pass

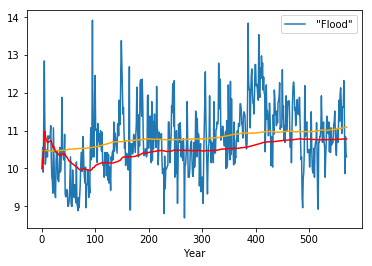

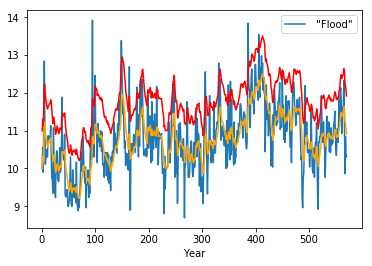

Expanding windows grow as the time series progresses¶

In [52]:

ts['expanding'] = ts.ts.expanding().sum()

ts

Out[52]:

| ts | rolling | expanding | |

|---|---|---|---|

| 0 | 0 | NaN | 0.0 |

| 1 | 1 | NaN | 1.0 |

| 2 | 2 | 3.0 | 3.0 |

| 3 | 3 | 6.0 | 6.0 |

| 4 | 4 | 9.0 | 10.0 |

In [53]:

df.plot()

plt.plot(df.expanding(center=True).mean(), c='orange')

plt.plot(df.expanding().mean(), c='red')

pass

Exponentially weighted windows place more weight on center of mass¶

In [54]:

n = 10

xs = np.arange(n, dtype='float')[::-1]

xs

Out[54]:

array([9., 8., 7., 6., 5., 4., 3., 2., 1., 0.])

Exponentially weighted windows without adjustment.

In [55]:

pd.Series(xs).ewm(alpha=0.8, adjust=False).mean()

Out[55]:

0 9.000000

1 8.200000

2 7.240000

3 6.248000

4 5.249600

5 4.249920

6 3.249984

7 2.249997

8 1.249999

9 0.250000

dtype: float64

Re-implementation for insight.

In [56]:

α = 0.8

ys = np.zeros_like(xs)

ys[0] = xs[0]

for i in range(1, len(xs)):

ys[i] = (1-α)*ys[i-1] + α*xs[i]

ys

Out[56]:

array([9. , 8.2 , 7.24 , 6.248 , 5.2496 ,

4.24992 , 3.249984 , 2.2499968 , 1.24999936, 0.24999987])

Exponentially weighted windows with adjustment (default)

In [57]:

pd.Series(xs).ewm(alpha=0.8, adjust=True).mean()

Out[57]:

0 9.000000

1 8.166667

2 7.225806

3 6.243590

4 5.248399

5 4.249616

6 3.249910

7 2.249980

8 1.249995

9 0.249999

dtype: float64

Re-implementation for insight.

In [58]:

α = 0.8

ys = np.zeros_like(xs)

ys[0] = xs[0]

for i in range(1, len(xs)):

ws = np.array([(1-α)**(i-t) for t in range(i+1)])

ys[i] = (ws * xs[:len(ws)]).sum()/ws.sum()

ys

Out[58]:

array([9. , 8.16666667, 7.22580645, 6.24358974, 5.24839949,

4.24961598, 3.2499104 , 2.24997952, 1.24999539, 0.24999898])

In [59]:

df.plot()

plt.plot(df.ewm(alpha=0.8).mean(), c='orange')

plt.plot(df.ewm(alpha=0.2).mean(), c='red')

pass

Alternatives to \(\alpha\)

Using span

Using halflife

Using com

In [60]:

df.plot()

plt.plot(df.ewm(span=10).mean(), c='orange')

plt.plot(1+ df.ewm(alpha=2/11).mean(), c='red') # offfset for visibility

pass

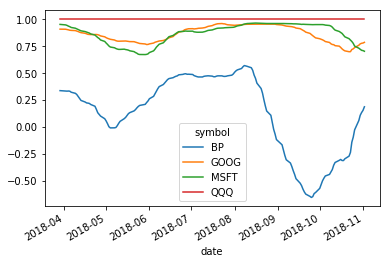

Correlation between time series¶

Suppose we had a reference time series. It is often of interest to know how any particular time series is correlated with the reference. Often the reference might be a population average, and we want to see where a particular time series deviates in behavior.

In [61]:

import pandas_datareader.data as web

We will look at the correlation of some stocks.

QQQ tracks Nasdaq

MSFT is Microsoft

GOOG is Gogole

BP is British Petroleum

We expect that the technology stocks should be correlated with Nasdaq, but maybe not BP.

In [62]:

df = web.DataReader(['QQQ', 'MSFT','GOOG', 'BP'], 'robinhood')

In [63]:

df = df[['close_price']]

In [64]:

df = df.unstack(level=0)

In [65]:

df.columns = df.columns.get_level_values(1)

In [66]:

df.index.name = 'date'

In [67]:

df.index = pd.to_datetime(df.index)

In [68]:

df.head()

Out[68]:

| symbol | BP | GOOG | MSFT | QQQ |

|---|---|---|---|---|

| date | ||||

| 2017-11-03 | 38.839900 | 1032.480000 | 82.643000 | 152.102400 |

| 2017-11-06 | 39.653900 | 1025.900000 | 82.967200 | 152.618500 |

| 2017-11-07 | 39.720900 | 1033.330000 | 82.770700 | 152.707800 |

| 2017-11-08 | 39.644300 | 1039.850000 | 83.055600 | 153.323100 |

| 2017-11-09 | 39.582200 | 1031.260000 | 82.593900 | 152.519200 |

In [69]:

df.rolling(100).corr(df.QQQ).plot()

pass

Visualizing space and time data¶

Being able to visualize events in space and time can be impressive. With Python, often you need a trivial amount of code to produce an impressive visualization.

For example, lets generate a heatmap of crimes in Sacramento in 2006, and highlight the crimes committed 10 seconds before midnight.

See the gmaps package for more information.

In [70]:

sacramento_crime = pd.read_csv('data/SacramentocrimeJanuary2006.csv', index_col=0)

In [71]:

sacramento_crime.index = pd.to_datetime(sacramento_crime.index)

In [72]:

sacramento_crime.head()

Out[72]:

| address | district | beat | grid | crimedescr | ucr_ncic_code | latitude | longitude | |

|---|---|---|---|---|---|---|---|---|

| cdatetime | ||||||||

| 2006-01-01 | 3108 OCCIDENTAL DR | 3 | 3C | 1115 | 10851(A)VC TAKE VEH W/O OWNER | 2404 | 38.550420 | -121.391416 |

| 2006-01-01 | 2082 EXPEDITION WAY | 5 | 5A | 1512 | 459 PC BURGLARY RESIDENCE | 2204 | 38.473501 | -121.490186 |

| 2006-01-01 | 4 PALEN CT | 2 | 2A | 212 | 10851(A)VC TAKE VEH W/O OWNER | 2404 | 38.657846 | -121.462101 |

| 2006-01-01 | 22 BECKFORD CT | 6 | 6C | 1443 | 476 PC PASS FICTICIOUS CHECK | 2501 | 38.506774 | -121.426951 |

| 2006-01-01 | 3421 AUBURN BLVD | 2 | 2A | 508 | 459 PC BURGLARY-UNSPECIFIED | 2299 | 38.637448 | -121.384613 |

In [73]:

gmaps.configure(api_key=os.environ["GOOGLE_API_KEY"])

In [74]:

locations = sacramento_crime[['latitude', 'longitude']]

In [75]:

late_locations = sacramento_crime.between_time('23:59', '23:59:59')[['latitude', 'longitude']]

In [76]:

fig = gmaps.figure()

fig.add_layer(gmaps.heatmap_layer(locations))

markers = gmaps.marker_layer(late_locations)

fig.add_layer(markers)

fig