Averaging and

smoothing models

Averaging and

smoothing models

Notes

on forecasting with moving averages (pdf)

Moving average and

exponential smoothing models

Slides

on inflation and seasonal adjustment and Winters seasonal exponential smoothing

Spreadsheet implementation of seasonal adjustment and

exponential smoothing

Equations

for the smoothing models (SAS web site)

Moving average and

exponential smoothing models

Simple moving average

model

Brown’s simple exponential smoothing model

Brown’s linear exponential smoothing model

Holt’s linear exponential smoothing model

As a first

step in moving beyond mean models, random walk models, and linear trend models,

nonseasonal patterns and trends can be extrapolated using a moving-average

or smoothing model. The basic assumption behind averaging and smoothing

models is that the time series is locally stationary with a slowly varying

mean. Hence, we take a moving (local) average to estimate the current

value of the mean and then use that as the forecast for the near future. This

can be considered as a compromise between the mean model and the

random-walk-without-drift-model. The same strategy can be used to estimate and

extrapolate a local trend. A moving

average is often called a "smoothed" version of the original series

because short-term averaging has the effect of smoothing out the bumps in the

original series. By adjusting the degree of smoothing (the width of the moving

average), we can hope to strike some kind of optimal balance between the

performance of the mean and random walk models. The simplest kind of averaging

model is the....

Simple

(equally-weighted) Moving Average:

The forecast

for the value of Y at time t+1 that is made at time t equals the simple average

of the most recent m observations:

![]()

(Here and elsewhere I will use the symbol

“Y-hat” to stand for a forecast of the time series Y made at the

earliest possible prior date by a given model.) This average is centered at period t-(m+1)/2, which

implies that the estimate of the local mean will tend to lag behind the true

value of the local mean by about (m+1)/2 periods. Thus, we say the average age of the data in the simple

moving average is (m+1)/2 relative to the period for which the forecast is

computed: this is the amount of time by which forecasts will tend to lag

behind turning points in the data. For example, if you are averaging the

last 5 values, the forecasts will be about 3 periods late in responding to

turning points. Note that if m=1, the simple moving average (SMA) model is

equivalent to the random walk model (without growth). If m is very large

(comparable to the length of the estimation period), the SMA model is

equivalent to the mean model. As with any parameter of a forecasting model, it

is customary to adjust the value of k in order to obtain the best "fit"

to the data, i.e., the smallest forecast errors on average.

Here is an example of a series which

appears to exhibit random fluctuations around a slowly-varying mean. First,

let's try to fit it with a random walk model, which is equivalent to a simple

moving average of 1 term:

The random

walk model responds very quickly to changes in the series, but in so doing it

picks much of the "noise" in the data (the random fluctuations) as

well as the "signal" (the local mean). If we instead try a simple

moving average of 5 terms, we get a smoother-looking set of forecasts:

The 5-term

simple moving average yields significantly smaller errors than the random walk

model in this case. The average age of the data in this forecast is 3

(=(5+1)/2), so that it tends to lag behind turning points by about three

periods. (For example, a downturn seems to have occurred at period 21, but the

forecasts do not turn around until several periods later.)

Notice that the long-term forecasts

from the SMA model are a horizontal straight line, just as in the

random walk model. Thus, the SMA model assumes that there is no trend in

the data. However, whereas the forecasts from the random walk model are simply

equal to the last observed value, the forecasts from the SMA model are equal to

a weighted average of recent values.

The confidence

limits computed by Statgraphics for the long-term forecasts of the simple

moving average do not get wider as the forecasting horizon increases.

This is obviously not correct! Unfortunately, there is no underlying

statistical theory that tells us how the confidence intervals ought to widen

for this model. However, it is not

too hard to calculate empirical

estimates of the confidence limits for the longer-horizon forecasts. For

example, you could set up a spreadsheet in which the SMA model would be used to

forecast 2 steps ahead, 3 steps ahead, etc., within the historical data sample.

You could then compute the sample standard deviations of the errors at each

forecast horizon, and then construct confidence intervals for longer-term

forecasts by adding and subtracting multiples of the appropriate standard

deviation.

If we try

a 9-term simple moving average, we get even smoother forecasts and more of a

lagging effect:

The

average age is now 5 periods (=(9+1)/2). If we take a 19-term moving average,

the average age increases to 10:

Notice

that, indeed, the forecasts are now lagging behind turning points by about 10

periods.

Which

amount of smoothing is best for this series? Here is a table that compares their

error statistics, also including a 3-term average:

Model C,

the 5-term moving average, yields the lowest value of RMSE by a small margin

over the 3-term and 9-term averages, and their other stats are nearly

identical. So, among models with

very similar error statistics, we can choose whether we would prefer a little

more responsiveness or a little more smoothness in the forecasts. (Return to top of page.)

Brown's

Simple Exponential Smoothing (exponentially weighted moving average)

The simple

moving average model described above has the undesirable property that it

treats the last k observations equally and completely ignores all preceding

observations. Intuitively, past data should be discounted in a more gradual

fashion--for example, the most recent observation should get a little more

weight than 2nd most recent, and the 2nd most recent should get a little more

weight than the 3rd most recent, and so on. The simple exponential smoothing

(SES) model accomplishes this.

Let α denote a "smoothing

constant" (a number between 0 and 1).

One way to write the model is to define a series L that represents the

current level (i.e., local mean value) of the series as estimated from data up

to the present. The value of

L at time t is computed recursively from its own previous value like this:

Lt

= αYt +

(1-α) Lt-1

Thus, the current smoothed value is an

interpolation between the previous smoothed value and the current observation,

where α controls the

closeness of the interpolated value to the most recent observation. The forecast

for the next period is simply the current smoothed value:

![]()

Equivalently, we can express the next

forecast directly in terms of previous forecasts and previous observations, in

any of the following equivalent versions.

In the first version, the forecast is an interpolation between previous forecast

and previous observation:

![]()

In the second version, the next forecast is

obtained by adjusting the previous forecast in the direction of the

previous error by a fractional amount

α:

![]()

where

![]()

is the error made at time t. In the third version, the forecast is an exponentially

weighted (i.e. discounted) moving average with discount factor 1-α:

![]()

The interpolation version of the

forecasting formula is the simplest to use if you are implementing the model on

a spreadsheet: it fits in a single cell and contains cell references pointing

to the previous forecast, the previous observation, and the cell where the

value of α is stored.

Note that

if α=1, the SES model

is equivalent to a random walk model (without growth). If α=0, the SES model is equivalent to the mean

model, assuming that the first smoothed value is set equal to the mean. (Return to top of page.)

The

average age of the data in the simple-exponential-smoothing forecast is 1/α relative to the

period for which the forecast is computed. (This is not supposed to be obvious,

but it can easily be shown by evaluating an infinite series.) Hence, the simple

moving average forecast tends to lag behind turning points by about 1/α periods. For example, when α=0.5 the lag is 2 periods; when α=0.2 the lag is 5 periods; when α=0.1 the lag is 10 periods, and so on.

For a

given average age (i.e., amount of lag), the simple exponential smoothing (SES)

forecast is somewhat superior to the simple moving average (SMA) forecast

because it places relatively more weight on the most recent observation--i.e.,

it is slightly more "responsive" to changes occuring in the recent

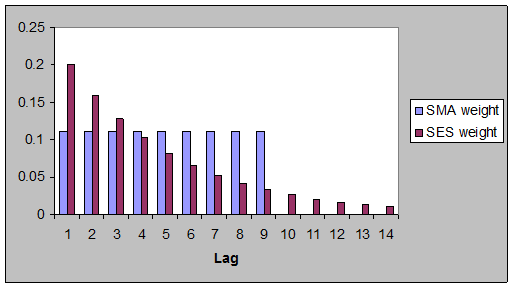

past. For example, an SMA model with 9 terms and an SES model

with α=0.2 both have an

average age of 5 for the data in their forecasts, but the SES model

puts more weight on the last 3 values than does the SMA model and at the same

time it doesn’t entirely “forget” about values more than 9

periods old, as shown in this chart:

![]()

Another

important advantage of the SES model over the SMA model is that the SES model

uses a smoothing parameter which is continuously variable, so it can easily

optimized by using a "solver" algorithm to minimize the mean squared

error. The optimal value of α in the SES model for this series turns out

to be 0.2961, as shown here:

The

average age of the data in this forecast is 1/0.2961 = 3.4 periods, which is

similar to that of a 6-term simple moving average.

The

long-term forecasts from the SES model are a horizontal straight line,

as in the SMA model and the random walk model without growth. However, note

that the confidence intervals computed by Statgraphics now diverge in a

reasonable-looking fashion, and that they are substantially narrower than the

confidence intervals for the random walk model. The SES model assumes that the

series is somewhat "more predictable" than does the random walk

model.

An SES

model is actually a special case of an ARIMA model, so the statistical

theory of ARIMA models provides a sound basis for calculating confidence

intervals for the SES model. In particular, an SES model is an ARIMA model

with one nonseasonal difference, an MA(1) term, and no constant term,

otherwise known as an "ARIMA(0,1,1) model without constant". The

MA(1) coefficient in the ARIMA model corresponds to the quantity 1-α in the SES model. For example, if you fit

an ARIMA(0,1,1) model without constant to the series analyzed here, the

estimated MA(1) coefficient turns out to be 0.7029, which is almost exactly one

minus 0.2961.

It is

possible to add the assumption of a non-zero constant linear trend to an

SES model. To do this, just specify an ARIMA model with one nonseasonal

difference and an MA(1) term with a constant, i.e., an ARIMA(0,1,1)

model with constant. The long-term forecasts will then have a trend

which is equal to the average trend observed over the entire estimation period.

You cannot do this in conjunction with seasonal adjustment, because the

seasonal adjustment options are disabled when the model type is set to

ARIMA. However, you can add a constant long-term exponential trend

to a simple exponential smoothing model (with or without seasonal adjustment)

by using the inflation adjustment option in the Forecasting

procedure. The appropriate "inflation" (percentage growth) rate

per period can be estimated as the slope coefficient in a linear trend model

fitted to the data in conjunction with a natural logarithm transformation, or

it can be based on other, independent information concerning long-term growth

prospects. (Return

to top of page.)

Brown's Linear (i.e., double)

Exponential Smoothing

The SMA models and SES models assume that there is no trend of any kind in the

data (which is usually OK or at least not-too-bad for 1-step-ahead forecasts when

the data is relatively noisy), and they can be modified to incorporate a

constant linear trend as shown above.

What about short-term trends?

If a series displays a varying rate of growth or a cyclical pattern that

stands out clearly against the noise, and if there is a need to forecast more

than 1 period ahead, then estimation of a local trend might also be an

issue. The simple exponential

smoothing model can be generalized to obtain a linear exponential smoothing (LES) model that computes local estimates of both level and

trend.

The simplest time-varying trend model is Brown's linear exponential

smoothing model, which uses two different smoothed series

that are centered at different points in time. The forecasting formula is based on an

extrapolation of a line through the two centers. (A more sophisticated version of

this model, Holt’s, is discussed below.)

The algebraic form of Brown’s linear exponential

smoothing model, like that of the simple exponential smoothing model, can be

expressed in a number of different but equivalent forms. The

"standard" form of this model is usually expressed as follows: Let S'

denote the singly-smoothed series obtained by applying simple

exponential smoothing to series Y. That is, the value of S' at period t is

given by:

![]()

(Recall that, under simple

exponential smoothing, this would be the forecast for Y at period t+1.) Then

let S" denote the doubly-smoothed series obtained by applying

simple exponential smoothing (using the same α) to series S':

![]()

Finally, the forecast for Yt+k, for any k>1, is given by:

![]()

where:

![]()

...is the estimated level at

period t, and

![]()

...is the

estimated trend at period t.

For purposes of model-fitting (i.e., calculating forecasts,

residuals, and residual statistics over the estimation period), the model can

be started up by setting S'1 =

S''1 = Y1, i.e., set both smoothed

series equal to the observed value at t=1.

(Return to top of page.)

A mathematically equivalent form of Brown's linear

exponential smoothing model, which emphasizes its non-stationary character and

is easier to implement on a spreadsheet, is the following:

![]()

or equivalently:

![]()

In other words, the predicted

difference at period t is equal to the previous observed difference minus

a weighted difference of the two previous forecast errors.

Caution: this form of the model is rather

tricky to start up at the beginning of the estimation period. The following

convention is recommended:

![]()

This yields e1 = 0 (i.e., cheat a bit, and let

the first forecast equal the actual first observation), and e2 =

Y2 – Y1, after which forecasts are generated

using the equation above. This yields the same fitted values as the formula

based on S' and S'' if the latter were started up using S'1 = S''1 =

Y1. This

version of the model is used on the next page that illustrates a combination of exponential

smoothing with seasonal adjustment.

Holt’s

Linear Exponential Smoothing

Brown’s LES model computes local

estimates of level and trend by smoothing the recent data, but the fact that it

does so with a single smoothing parameter places a constraint on the data

patterns that it is able to fit:

the level and trend are not allowed to vary at independent rates. Holt’s LES model addresses this

issue by including two smoothing

constants, one for the level and one for the trend. At any time t, as in Brown’s

model, the there is an estimate Lt of the local level and an

estimate Tt of the local trend.

Here they are computed recursively from the value of Y observed at time

t and the previous estimates of the level and trend by two equations that apply

exponential smoothing to them separately.

If the estimated level and trend at time

t-1 are Lt‑1 and Tt-1, respectively, then the

forecast for Yt that would have been made at time t-1 is equal

to Lt-1+Tt-1.

When the actual value is observed, the updated estimate of the level is

computed recursively by interpolating between Yt and its

forecast, Lt-1+Tt-1, using weights of α and 1-α:

![]()

The change in the estimated level, namely Lt

‑ Lt‑1, can be interpreted as a noisy measurement

of the trend at time t. The updated

estimate of the trend is then computed recursively by interpolating between Lt

‑ Lt‑1 and the previous estimate of the trend, Tt-1,

using weights of β and 1-β:

![]()

Finally, the forecasts for the near future

that are made from time t are obtained by extrapolation of the updated level

and trend:

![]()

The interpretation of the trend-smoothing

constant β is analogous to that of the level-smoothing constant

α. Models with small values of β

assume that the trend changes only very slowly over time, while models with

larger β assume that it is changing more rapidly. A model with a large β believes

that the distant future is very uncertain, because errors in trend-estimation

become quite important when forecasting more than one period ahead. (Return to top of page.)

The smoothing constants α and β can be

estimated in the usual way by minimizing the mean squared error of the

1-step-ahead forecasts. When this

done in Statgraphics, the estimates turn out to be α =0.3048 and β

=0.008. The very small value of

β means that the model assumes very little change in the trend from one

period to the next, so basically this model is trying to estimate a long-term

trend. By analogy with the

notion of the average age of the data that is used in estimating the local

level of the series, the average age of the data that is used in estimating the

local trend is proportional to 1/ β, although not exactly equal to it. In

this case that turns out to be 1/0.006 = 125. This isn’t a very precise number

inasmuch as the accuracy of the estimate of β isn’t really 3 decimal

places, but it is of the same general order of magnitude as the sample size of

100, so this model is averaging over quite a lot of history in estimating the

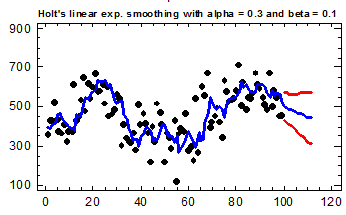

trend. The forecast plot

below shows that the LES model estimates a slightly larger local trend at the

end of the series than the constant trend estimated in the SES+trend

model. Also, the estimated value of

α

is almost identical to the one obtained by fitting the SES model with or

without trend, so this is almost the same model.

Now, do these look like reasonable

forecasts for a model that is supposed to be estimating a local trend? If you “eyeball” this plot,

it looks as though the local trend has turned downward at the end of the

series! What has happened? The parameters of this model have been estimated

by minimizing the squared error of 1-step-ahead forecasts, not longer-term

forecasts, in which case the trend doesn’t make a lot of difference. If all you are looking at are

1-step-ahead errors, you are not seeing the bigger picture of trends over (say)

10 or 20 periods. In order to get

this model more in tune with our eyeball extrapolation of the data, we can

manually adjust the trend-smoothing constant so that it uses a shorter baseline

for trend estimation. For

example, if we choose to set β =0.1, then the average age of the data used

in estimating the local trend is 10 periods, which means that we are averaging

the trend over that last 20 periods or so.

Here’s what the forecast plot looks like if we set β =0.1

while keeping α

=0.3. This looks intuitively

reasonable for this series, although it is probably dangerous to extrapolate this

trend any more than 10 periods in the future.

What about the error stats? Here is a model comparison for the two

models shown above as well as three SES models. The optimal value of α.for the SES model

is approximately 0.3, but similar results (with slightly more or less

responsiveness, respectively) are obtained with 0.5 and 0.2.

Models

(A) Holt's linear exp. smoothing with alpha = 0.3048

and beta = 0.008

(B) Holt's linear exp. smoothing with alpha = 0.3 and

beta = 0.1

(C) Simple exponential smoothing with alpha = 0.5

(D) Simple exponential smoothing with alpha = 0.3

(E) Simple exponential smoothing with alpha = 0.2

Estimation Period

|

Model |

RMSE |

MAE |

MAPE |

ME |

MPE |

|

(A) |

98.9302 |

76.3795 |

16.418 |

-6.58179 |

-7.0742 |

|

(B) |

100.863 |

78.3464 |

16.047 |

-3.78268 |

-5.63482 |

|

(C) |

101.053 |

76.7164 |

14.605 |

1.70418 |

-4.94903 |

|

(D) |

98.3782 |

75.0551 |

18.9899 |

3.21634 |

-4.85287 |

|

(E) |

99.5981 |

76.3239 |

12.528 |

5.20827 |

-4.7815 |

|

Model |

RMSE |

RUNS |

RUNM |

AUTO |

MEAN |

VAR |

|

(A) |

98.9302 |

OK |

OK |

OK |

OK |

OK |

|

(B) |

100.863 |

OK |

OK |

OK |

OK |

OK |

|

(C) |

101.053 |

OK |

OK |

OK |

OK |

OK |

|

(D) |

98.3782 |

OK |

OK |

OK |

OK |

OK |

|

(E) |

99.5981 |

OK |

* |

OK |

OK |

OK |

Their

stats are nearly identical, so we really can’t make the choice on the

basis of 1-step-ahead forecast errors within the data sample. We have to fall back on other

considerations. If we strongly

believe that it makes sense to base the current trend estimate on what has

happened over the last 20 periods or so, we can make a case for the LES model

with α

= 0.3 and β = 0.1. If we want

to be agnostic about whether there is a local trend, then one of the SES models

might be easier to explain and would also give more middle-of-the-road

forecasts for the next 5 or 10 periods.

(Return to top of page.)

Which type of

trend-extrapolation is best: horizontal or linear? Empirical evidence

suggests that, if the data have already been adjusted (if necessary) for

inflation, then it may be imprudent to extrapolate short-term linear trends

very far into the future. Trends evident today may slacken in the future due to

varied causes such as product obsolescence, increased competition, and cyclical

downturns or upturns in an industry. For this reason, simple exponential

smoothing often performs better out-of-sample than might otherwise be expected,

despite its "naive" horizontal trend extrapolation. Damped trend modifications of the

linear exponential smoothing model are also often used in practice to introduce

a note of conservatism into its trend projections. The damped-trend LES model can be

implemented as a special case of an ARIMA model, in particular, an ARIMA(1,1,2) model.

It is possible to

calculate confidence intervals around long-term forecasts produced by

exponential smoothing models, by considering them as special cases of ARIMA models. (Beware: not all software calculates

confidence intervals for these models correctly.) The width of the confidence intervals

depends on (i) the RMS error of the model, (ii) the type of smoothing (simple

or linear); (iii) the value(s) of

the smoothing constant(s); and (iv) the number of periods ahead you are forecasting.

In general, the intervals spread out faster as α gets larger in the

SES model and they spread out much faster when linear rather than simple

smoothing is used. This topic is

discussed further in the ARIMA models section of the notes. (Return to top of page.)

Go on to next topic: spreadsheet implementation of seasonal

adjustment and exponential smoothing