Simple forecasting models

Simple forecasting models

Statistics

review and the simplest forecasting model: the sample mean (pdf)

Notes on the random

walk model (pdf)

Mean (constant) model

Linear trend model

Random walk model

Geometric random walk model

Three types of forecasts: estimation, validation, and the

future

Random walk model

When faced

with a time series that shows irregular growth, such as X2 analyzed earlier, the best strategy

may not be to try to directly predict the level of the series at each

period (i.e., the quantity Yt). Instead, it may

be better to try to predict the change that occurs from one period to

the next (i.e., the quantity Yt - Yt-1). That is, it may be better to look at the

first difference of the series, to see if a

predictable pattern can be found there. For purposes of one-period-ahead

forecasting, it is just as good to predict the next change as to predict the

next level of the series, since the predicted change can be added to the

current level to yield a predicted level. The simplest case of such a model is

one that always predicts that the next change will be zero, as if the series is

equally likely to go up or down in the next period regardless of what it has

done in the past.

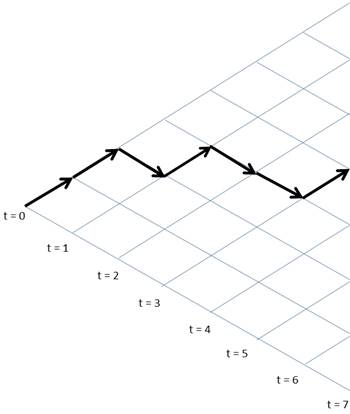

Here's a

picture that illustrates a random process for which this model is appropriate:

In each

time period, going from left to right, the value of the variable takes an

independent random step up or down, a so-called random walk. If up and down movements are equally likely at each

intersection, then every possible left-to-right path through the grid is

equally likely a priori. See this

link for a nice simulation. A commonly-used analogy is that of a drunkard

who staggers randomly to the left or right as he tries to go forward: the path

he traces will be a random walk.

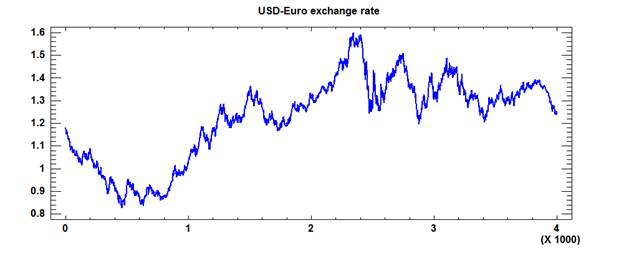

For

a real-world example, consider the daily US-dollar-to-Euro exchange rate. A

plot of its entire history from January 1, 1999, to December 5, 2014 (4006

observations) looks like this:

The historical

pattern looks quite interesting, with many peaks and valleys.

("Chartists" often try to extrapolate such patterns by fitting local

trend lines or curves, which I do not recommend. On average, 49% of them will correctly

guess the direction in which the market will move between today and some given

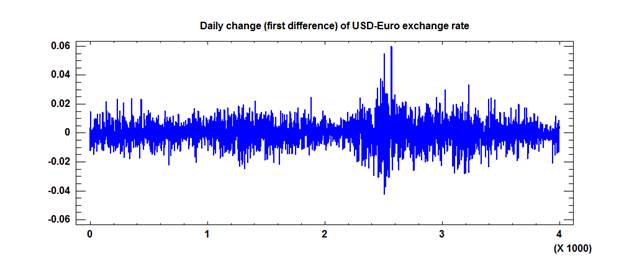

future date.) Now, here's a plot of the daily changes (first difference):

The

volatility (variance) has not been constant over time, but the day-to-day

changes are almost completely random, as shown by a plot of their autocorrelations:

The autocorrelation at lag k is the

correlation between the variable and itself lagged by k periods. If the values in

the series are completely random in the sense of being statistically

independent, the true values of the autocorrelations are zero, and the

estimated values should not be significantly different from zero. The red lines

on this plot are significance bands for testing whether the autocorrelations of

the daily changes are different from zero at the 0.05 level of significance,

and overall they are not. In particular, they are completely insignificant at

the first few lags and there is no systematic pattern. (For large samples,

autocorrelations are significantly different from zero at the 0.05 level if

their magnitude exceeds plus-or-minus two

divided by the square root of the sample size. Here the sample size is

4006, and 2/SQRT(4006) is approximately 0.03, as seen in the location of the

red lines on the plot.)

The

forecasting model suggested by these plots is one that merely predicts no change from the one period to the

next, because past data provides no information about the direction of future

movements:

Ŷt = Yt-1

This is

the so-called random-walk-without-drift

model: it assumes that, at each point in time, the series merely takes a

random step away from its last recorded position, with steps whose mean value

is zero. If the mean step size is some nonzero value α, the process is

said to be a random-walk-with-drift, whose prediction

equation is Ŷt = Yt-1 + α. The drunkard in

the picture above is missing one shoe, so he was probably drifting.

In general

the steps could be be discrete or continuous random variables, and the time

scale could also be discrete or continuous. Random walk patterns are commonly

seen in price histories of financial assets for which speculative markets

exist, such as stocks and currencies. This does not mean that movements in

those prices are random in the sense of being without purpose. When they go up

and down, it is always for a reason! But the direction of the next move cannot

be predicted ex ante: it can only be explained ex post, because if the

direction and magnitude of the next price movement could have been predicted in

advance, then speculators would already have bid it up or down by that amount.

Random walk patterns are also widely found elsewhere in nature, for example, in

the phenomenon of Brownian

motion that was first explained by Einstein. (Return to top

of page.)

It is

difficult to tell whether the mean step size in a random walk is really zero,

let alone estimate its precise value, merely by looking at the historical data

sample. If you simulate a random walk process (for example, by building a

spreadsheet model that uses the RAND() function in the formula for generating

the step values), you will typically find that different iterations of the same

model will yield dramatically different pictures, many of which will have

significant-looking trends, as shown in the simulation

link mentioned above. In fact, the same model will usually yield both

upward and downward trends in repeated iterations, as well as

interesting-looking curves that seem to demand some sort of complex model. This

is just a statistical illusion, like the so-called "hot hand in

basketball" and other examples of "streakiness" in sports. Your

brain tries hard to find patterns, even when they are not there. See the Hot Hand in Sports web site for more

on this.

In

applications, it is best to draw on other sources of information and on

theoretical considerations in deciding whether to include a drift term in the

model, and if so, how to estimate its value. In the case of exchange rates,

there is no reason to assume a long-term trend in one direction or the other,

at least, not a trend that would stand out against the noise. The mean daily

change is 0.000012 for this sample of exchange rate data, and the standard

error of the mean is 0.00012, so the sample mean is different from zero by only

1/10th of a standard error, which is not significant by any measure.

Again, though, the mean value of the steps in a finite sample of random-walk

data generally does not provide a good estimate of the current rate of drift,

if any.

Overall,

then, it appears that a random-walk-without-drift model is appropriate for this

time series. If the model is fitted to the entire history of the daily data,

going back to 1999, the forecasts and 50% confidence limits produced by the

model look like this:

(This

chart was produced by Statgraphics. 50% rather than 95% limits are shown merely

to make them fit better in the picture. There is nothing special about 95%

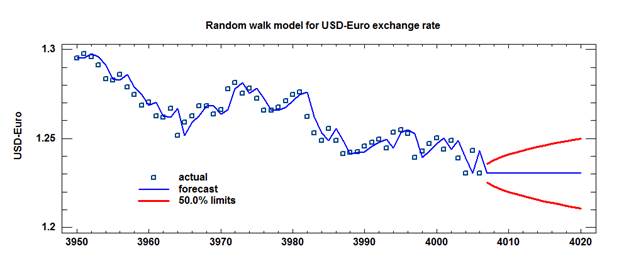

anyway, apart from convention.) Here is a close-up view of the actual data

points and forecasts at the very end of the series:

The key

properties of the model that are illustrated by this graph are the following:

a. The one-step-ahead forecasts within the sample

follow exactly the same path as the data, except that they lag behind by one period. (You must look

carefully to see this: at first glance it may appear that the model fits the

data perfectly, but in fact it is making errors in every period, and those

errors are independent random variables.)

b. The long-term forecasts outside the sample

follow a horizontal straight line anchored on the last observed value,

because no upward or downward drift or any other systematic time pattern is

assumed. (If non-zero drift was assumed, this line might slope upward or downward.)

c. The confidence bands for long-term forecasts grow

wider in a fashion that looks like a sideways

parabola, for reasons explained below. (Return to top of

page.)

In the

random-walk-without-drift model, the standard error of the 1-step ahead forecast

is the root-mean-squared-value of the period-to-period changes in the data

sample, i.e., it is the square root of the average of squared values of the

first difference of the series. For a random-walk-with-drift, the forecast standard error is the sample standard deviation of the period-to-period changes. (The

difference between the RMS value and the standard deviation of the changes is

usually negligible unless the volatility is very small in comparison to the

drift.)

The error

that the model makes in a k-step-ahead

forecast is the sum of k independently and identically distributed random

variables, because the model continues to make the same prediction while the

variable takes k random steps. Because the variance of a sum of independent

random variables is the sum of the variances, it follows that the variance of

the k-step-ahead forecast error is larger than that of the one-period-ahead

forecast by a factor of k. And because the standard deviation of the forecast

error is the square root of its variance, it follows that the standard error of a k-step-ahead forecast

is larger than that of the 1-step-ahead forecast by a factor of

square-root-of-k. This is the so-called "square root of time"

rule for the errors of random walk forecasts, and it explains the

sideways-parabola shape of the confidence bands for long-term forecasts: that's

the shape of the graph of Y=SQRT(X).

For this

very large data sample, the root-mean-squared value and the sample standard

deviation of the daily changes are both equal to 0.00778 to 3 significant

digits, so the standard error of a k-step ahead forecast error is

0.00778*SQRT(k), and confidence limits are calculated from it in the usual way.

A 95% interval is (approximately) the point forecast plus-or-minus 2 standard

errors, and a 50% confidence interval is the point forecast plus-or-minus

two-thirds of a standard error.

In the

case of the exchange rate data, it is not really appropriate to use the entire

sample to estimate the standard deviation of the daily changes, because it

clearly has not been constant over time. A shorter data history could be used

to address this problem, and other kinds of information such as prices of

foreign-exchange options could also be considered.

The random

walk model may look trivial if you have never seen it before: what could be

more simple-minded than always predicting that tomorrow will be the same as

today? This does not even require any knowledge of statistics! For that reason

it is sometimes called the "naive model." It is not at all trivial,

however. The square-root-of-time pattern in its confidence bands for long-term

forecasts is of profound importance in finance (it is the basis of the theory

of options pricing), and the random walk model often provides a good benchmark

against which to judge the performance of more complicated models.

The random

walk model can also be viewed as an important special case of an ARIMA model ("autoregressive

integrated moving average"). Specifically, it is an

"ARIMA(0,1,0)" model. More general ARIMA models are capable of

dealing with more interesting time patterns that involve correlated steps, such

as mean reversion, oscillation, time-varying means, and seasonality. These

topics are discussed in detail in the ARIMA pages of these notes.

For a much more

complete discussion of the random walk model, illustrated by a shorter sample

of the exchange rate data, see the "Notes on the random

walk model" handout.