Simple forecasting models

Simple forecasting models

Statistics

review and the simplest forecasting model: the sample mean (pdf)

Notes on the random

walk model (pdf)

Mean (constant) model

Linear trend model

Random walk model

Geometric random

walk model

Three types of forecasts: estimation, validation, and the

future

Geometric random walk model

Logarithm

transformations of stock price data: Previously we saw that a

random-walk-without-drift model was capable of describing a financial time

series with no long-term trend and relatively constant volatility in absolute

terms (at least over the long run). What if the series displays an overall exponential trend and increasing volatility in absolute terms?

For example, here is a plot of the monthly closing values of the S&P 500

stock index from January 1980 to November 2014, showing consistent exponential

growth in the early years followed by the two (three?) market bubbles.

If we take

the first difference (monthly change) of this series, we obtain a series that

shows much higher variance during periods when the level was high:

These two

pictures suggest that the growth rate and random fluctuations may be more

consistent over time in percentage terms than in absolute terms. We can

linearize the exponential growth in the original series, and also stabilize the

variance of the monthly changes, by applying a natural

logarithm transformation.

Here's what it yields:

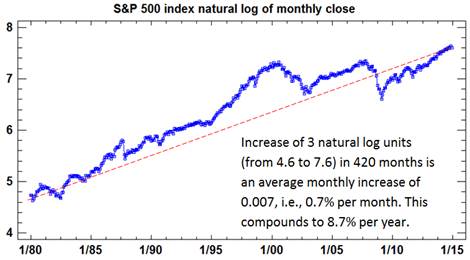

The growth

pattern now appears much more linear, although it has not been very consistent

in this wild-west era of epic bubbles and busts. As explained in the notes on the natural

log transformation, a trend measured in natural log units can be interpreted as

a trend measured in percentage terms, to a very high degree of approximation,

if it is on the order 5% or less per period. Here, a trend line has been hand-drawn

on the chart merely for visual reference, and it shows that the logged S&P

500 index has increased by about 3 units over the 420 months in the sample,

translating into an average monthly increase of 0.007, which can be interpreted

as 0.7% and which compounds to around 8.7% per year.

The

variance of the monthly changes also appears much more stable in log units, as

shown by a plot of the first difference of the logged series (its

"diff-log"):

The first

difference of the natural logarithm is essentially the percentage difference in the original series,

so what we have actually plotted here is the monthly percent return on

the S&P500 index (ex-dividends), and it generally falls in the range

between plus-and-minus 0.05, i.e., 5%. Its standard deviation is 0.044,

i.e., 4.4%.

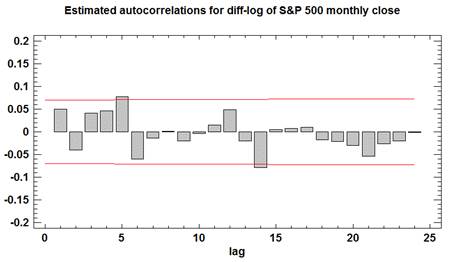

Finally,

let's check to see whether the diff-logged values are statistically

independent. Here is a plot of

their autocorrelations and 95% confidence bands around zero:

The

autocorrelations of the diff-logged series do not appear significant and do not

show any systematic pattern, from which we can conclude that the logged S&P 500 monthly closing

values can be reasonably described as a

random walk with drift.

When the

random-walk-with-drift model is fitted to the logged data, the point forecasts

and their 95% confidence limits for the next 3 years look like this:

The point

forecasts follow a straight line and the confidence bands for long term

forecasts have the characteristic sideways-parabola shape and are symmetric

around the point forecasts. The

drift has been estimated from the data sample in this case. This does not mean that a trend line has

been fitted by the usual regression method. Rather, it is as if a straight line was

drawn between the first and last data points and extrapolated from there. (That is the mathematical consequence of

applying the mean model to the diff-logged values: within the given data sample, the average

change from one period to the next is just the total change divided by the

number of time periods over which it occurred.) The dashed line on the above

plot has been added to emphasize this fact. It is apparent that this method of

estimating the drift could have yielded very different results if a different

amount of history had been used.

For example, if the starting point had been the peak of the dot-com

bubble, in August 2000, an extrapolation of a straight line through the first

and last points would have looked like this instead:

The level

of the series only increased by 0.28 log units over these 172 months (from 7.32

to 7.6), translating into 0.00165 per month (i.e., 0.165% per month), which

compounds to only 2% per year! On

the other hand, if you measure the growth rate over the 70-month period

starting from the bottom of the housing bust in March 2009, you get a much more

optimistic estimate of 19% per year:

This is why

it can be dangerous to estimate the average rate of return to be expected in

the future (let alone anticipate short-term changes in direction), by fitting

straight lines to finite samples of data.

Geometric

random walk model:

Application of the random walk model

to the logged series implies that the forecast for the next month's value of

the original series will equal the previous month's value plus a constant percentage

increase. To see this, note that the random walk forecast for LN(Y) is given by

the equation:

LN(Ŷt) = LN(Yt-1)

+ α

where the

constant term (alpha) is the average monthly change in LN(Y), which is

approximately the average monthly percentage change in Y. For the

S&P 500 series, alpha is equal to 0.007, representing an average monthly

increase of 0.7%. Exponentiating both sides of the preceding equation, and

using the fact that EXP(x) is approximately equal to 1+x for small x, we

obtain:

Ŷt = Yt-1 X EXP(α) ≈ Yt-1 X (1 + α)

This

forecasting model is known as a geometric random walk model, and it is

the default model commonly used for stock market data. (In Statgraphics, you

specify this model as a random-walk-with-growth model in combination with a

natural log transformation. On the Model

Specification panel in the user-specified forecasting procedure, just click

the "Random walk" button for the model type and the "Natural

log" button for the math adjustment, and check the "Constant"

box to incorporate constant growth.) Here's a plot of the forecasts produced by

this model for the S&P 500 series:

{kind=link}

This

picture is the same as the previous one except for the unlogging of the

vertical scale. The forecasts grow

at a rate equal to the average monthly increase within the sample, which is

0.7%, translating into 8.7% per year as noted earlier. In unlogged units, the 95% confidence

limits for long-term forecasts are noticeably asymmetric, being wider on the

high side.

For a much more

complete discussion of the geometric random walk model, see the "Notes

on the random walk model" handout.

A

"random walk down Wall Street": The fact

that stock prices behave at least approximately like a (geometric) random walk

is the most striking empirical fact about financial markets. But is it or

isn't it a true random walk? If it is, then stock prices are inherently

unpredictable except in terms of long-run-average risk and return. The

best you can hope to do is to correctly estimate the average returns and

volatilities of stocks, along with their correlations, and use these statistics

to determine efficient portfolios that achieve a desired risk-return

tradeoff. You can't hope to beat the market by microanalyzing patterns in

stock price movements--you might as well buy-and-hold an efficient portfolio.

The random

walk hypothesis was first formalized by the French mathematician (and stock

analyst) Louis Bachelier in 1900, and in the past century it has been

exhaustively studied and debated. The intuition for the random walk

hypothesis is a variation on the economist's classical efficiency argument,

which holds that a $100 bill will never be found lying on the sidewalk because

someone else would have picked it up first. If it could be predicted from

publicly available information that an abnormally large positive stock return

will occur tomorrow, then the price of the stock should already have gone up

today, in which case the anticipated return would already have been realized,

and tomorrow's return should be normal after all. What is not quite so

obvious is why the volatility of stock returns should be approximately

constant, as the basic random walk model assumes. (It is not exactly

constant in practice, but it does tend to revert to an average volatility

level over the long term.) Evidently investors naturally think in terms

of percentage changes when it comes to financial asset prices, so that

similar informational events (earnings reports, changes in interest rates or

inflation, etc.) tend to lead to similar percentage changes in stock prices at

different points in time.

Nowadays,

three different forms of the random walk hypothesis are commonly

distinguished. The weak form holds that future stock returns

cannot be predicted from past returns (except in the long-run-average sense),

which rules out so-called "technical analysis" and stock-trading

strategies such as "filter rules" in which buying and selling are

triggered when stock prices hit target levels determined by recent highs and

lows. The semi-strong form holds that future stock returns cannot

be predicted from past returns even together with other publicly available

information such as corporate statements and analyst reports, which rules

out the possibility that actively managed mutual funds will outperform a broad

market index (except by luck). The strong form holds that stock

returns cannot be predicted from any available information, even inside

information not available to the general public, which rules out excess profits

from insider trading. The strong form is obviously too strong to be

plausible: prices are moved by information (as well as by animal spirits,

etc.), and those who are able to trade on the information first, before

prices have moved very much, should expect to profit. The

general consensus seems to be that the truth lies somewhere between the

semi-strong and the strong form: technical analysis has not been

validated in controlled studies (although it still has passionate defenders),

and actively managed mutual funds generally do not consistently outperform the

market index, although inside information does create opportunities for

(illegal) excess profits.

On

reflection, it is intuitively reasonable that stock prices should follow a

random walk approximately, but not exactly. Small-scale patterns in stock

prices should always be emerging and then dissipating as information is

received by the most alert and savvy market participants, who then trade on it

until the rest of the market catches on. However, because of market

frictions (transaction costs such as bid-ask spreads, brokerage fees, taxes,

etc.), these patterns will usually be too small for the typical market observer

to profit from. For most practical purposes, for most people, it is

a random walk. This is not to say the market moves up or down for

purely random reasons. Looking backward, it is usually possible to

identify sound economic reasons for particular historical movements of stock

prices (notwithstanding the occasional speculative bubble like the dot-com

craze of the late 1990's). But looking forward, expectations of

future returns are already factored into today's prices, just so that future

returns will be average if today's expectations are exactly met. To the

extent that future returns deviate from the average, it will be due to the

occurrence of unanticipated events, which by definition are random deviations

from today's expectations.

The debate

between "technicians" and "random-walkers" has taken a new

turn with the emergence of behavioral finance as a lively field of study.

Behavioral finance studies markets from the perspective that investors are not

rational in the expected-utility-maximizing sense of classical finance theory,

as laboratory experiments have convincingly shown, which suggests that

psychological theories might be helpful in explaining some of the puzzles that

are observed in markets. On this view, reading stock charts might help to

anticipate the patterns that other people are likely to read into stock

charts. (The idea that markets are better predicted by psychological

analysis than by rational economic calculations, analogous to guessing the

winner of a beauty contest, actually dates back to John Maynard Keynes.)

But on the other hand, behavioral research has also convincingly demonstrated

that people tend to misperceive random sequences as non-random--the so-called

"hot hand in basketball" phenomenon. For more discussion of the

random walk hypothesis and its implications for investing, see A Random

Walk Down Wall Street by Burton Malkiel. (The latest

edition was published in 2012.) (Return to top of

page.)

More

general random walk forecasting models: For purposes of time series

forecasting, three versions of the random walk model can also be

distinguished. RW model 1 (the basic geometric random walk model illustrated

above and implementable in Statgraphics) assumes that stock returns in

different periods are statistically independent (uncorrelated) and also identically

distributed--i.e. the market has constant volatility. The only

parameters to estimate are the average period-to-period return (the constant

term in the ARIMA(0,1,0) model) and the volatility (the so-called white

noise standard deviation in the ARIMA(0,1,0) model, which is just ARIMA

jargon for root-mean-squared error). RW model 2 assumes that

returns in different periods are statistically independent but not

identically distributed--for example, the volatility might change

deterministically over time or it might depend on the current price level,

which would require more parameters to specify. RW model 3 assumes

that returns in different periods are uncorrelated but not

otherwise independent--e.g., the volatility in one period might depend on the

volatility in recent periods. The ARCH (autoregressive conditional

heteroscedasticity) and GARCH (generalized ARCH) models assume that the

local volatility follows an autoregressive process, which is

characterized by sudden jumps in volatility with a slow reversion to an average

volatility. The autoregressive behavior of volatility is clearly evident

in plots of returns over long periods, particularly high-frequency returns such

as daily returns. Robert Engle received the Nobel Prize in

Economics in 2003 for developing the ARCH model, and it is commonly used by

econometricians, although it is not available in Statgraphics. Subjective

estimates of time-varying volatilities are also revealed by prices of

derivative securities such as options: the "implied volatility"

of a stock price at a given point in time can be determined from stock options

prices using an options pricing model such as the Black-Scholes model.

What

does the empirical data show? Besides time-varying volatility, there is

some evidence for positive autocorrelation ("momentum") in some

stock price data, particularly at high frequencies (e.g. daily).

The history of daily returns on the S&P500 index and the Dow Jones

Industrial Average over the last 50 years shows a slight but technically

significant positive autocorrelation at lag 1, although this pattern seems to have

faded in recent decades. (Perhaps it self-destructed?) Other

patterns have also been observed to arise in some decades and fade away in

others. The behavior of the CRSP index (a common benchmark for

econometricians) is even more remarkable: daily returns on the CRSP

value-weighted index and equal-weighted index displayed lag-1 autocorrelations

in the range of 30% to over 40% over the period 1962-1978, and slightly less

over the larger period 1962-1994. This is remarkable not only for the

very large magnitude of the autocorrelations but also for the fact that returns

on individual stocks in the sample typically displayed no autocorrelation.

One explanation of this puzzle is that there appear to be significant cross-correlations

(also called "cross-auto-correlations") between different

segments of the market--e.g., some stocks tend to lead or lag others, as though

information diffuses across the market from one day to the next, even though

individually they behave like random walks. Thus, for example, stocks A and

B could both have zero autocorrelation at lag 1, but A could have a significant

lag-1 cross-correlation with stock B, and a portfolio formed of A plus B could

therefore have significant autocorrelation at lag 1. The question remains

whether this pattern is (or was) significant enough to present opportunities

for excess profits. Transaction costs make it difficult to profit from

trades in large numbers of stocks at once, unless the index is itself a traded

asset. If there were an asset pegged to the same CRSP index used in these

studies, the autocorrelation pattern might have been expected to

self-destruct. So, there are some predictable patterns in stock

prices (particularly at the aggregate level, and seen in hindsight), but the

returns on individual assets that can be traded with low transaction costs are

in reasonable agreement with RW model 3, if not one of the more restrictive

models. For more information (at a much higher technical level), see The

Econometrics of Financial Markets by John Campbell, Andrew Lo, and A. Craig

MacKinlay. (Return

to top of page.)