ARIMA models for time series forecasting

ARIMA models for time series forecasting

Notes

on nonseasonal ARIMA models (pdf file)

Slides on seasonal and

nonseasonal ARIMA models (pdf file)

Introduction

to ARIMA: nonseasonal models

Identifying the order of differencing in an ARIMA model

Identifying the numbers of AR or MA terms in an ARIMA

model

Estimation of ARIMA models

Seasonal differencing in ARIMA models

Seasonal random walk: ARIMA(0,0,0)x(0,1,0)

Seasonal random trend: ARIMA(0,1,0)x(0,1,0)

General seasonal models: ARIMA (0,1,1)x(0,1,1) etc.

Summary of rules for

identifying ARIMA models

ARIMA models with

regressors

The

mathematical structure of ARIMA models (pdf file)

ARIMA models with

regressors

An ARIMA

model can be considered as a special type of regression model--in which the

dependent variable has been stationarized and the independent variables are all

lags of the dependent variable and/or lags of the errors--so it is

straightforward in principle to extend an ARIMA model to incorporate

information provided by leading indicators and other exogenous variables: you

simply add one or more regressors to the forecasting equation.

Alternatively,

you can think of a hybrid ARIMA/regression model as a regression model which

includes a correction for autocorrelated errors. If you have fitted a multiple

regression model and find that its residual ACF and PACF plots display an

identifiable autoregressive or moving-average "signature" (e.g., some

significant pattern of autocorrelations and/or partial autocorrelations at the

first few lags and/or the seasonal lag), then you might wish to consider adding

ARIMA terms (lags of the dependent variable and/or the errors) to the

regression model to eliminate the autocorrelation and further reduce the mean

squared error. To do this, you would just re-fit the regression model as an

ARIMA model with regressors, and you would specify the appropriate AR and/or MA

terms to fit the pattern of autocorrelation you observed in the original

residuals.

Most

high-end forecasting software offers one or more options for combining the

features of ARIMA and multiple regression models. In the Forecasting procedure

in Statgraphics, you can do this by specifying "ARIMA" as the model

type and then hitting the "Regression" button to add regressors.

(Alas, you are limited to 5 additional regressors.) When you add a regressor to

an ARIMA model in Statgraphics, it literally just adds the regressor to the

right-hand-side of the ARIMA forecasting equation. To use a simple case,

suppose you first fit an ARIMA(1,0,1) model with no regressors. Then the

forecasting equation fitted by Statgraphics is:

Ŷt = μ + ϕ1Yt-1 -

θ1et-1

which can

be rewritten as:

Ŷt - ϕ1Yt-1 = μ - θ1et-1

(Note:

this is a standard mathematical form which is often used for ARIMA models. All

terms involving the dependent variable--i.e., all the AR terms and

differences--are collected on the left-hand-side of the equation, while all

terms involving the erorrs--i.e., the MA terms--are collected on the right-hand

side.) Now, if you add a regressor X to the forecasting model, the equation

fitted by Statgraphics is:

Ŷt - ϕ1Yt-1 = μ - θ1et-1 + β(Xt - ϕ1Xt-1)

Thus, the

AR part of the model (and also the differencing transformation, if any) is

applied to the X variable in exactly the same way as it is applied to the Y

variable before X is multiplied by the regression

coefficient. This effectively means that the ARIMA(1,0,1) model is

fitted to the errors of the regression of Y on X (i.e., the series "Y

minus beta X").

How can

you tell if it might be helpful to add a regressor to an ARIMA model? One

approach would be to save the RESIDUALS of the ARIMA model and then look at

their cross-correlations with other potential explanatory variables. For

example, recall that we previously fitted a regression model model to

seasonally adjusted auto sales, in which the LEADIND variable (index of eleven

leading economic indicators) turned out to be slightly significant in addition

to lags of the stationarized sales variable. Perhaps LEADIND would also be

helpful as a regressor in the seasonal ARIMA model we

subsequently fitted to auto sales.

To test

this hypothesis, the RESIDUALS from the ARIMA(0,1,1)x(0,1,1) model fitted to

AUTOSALE were saved. Their cross-correlations with DIFF(LOG(LEADIND)), plotted

in the Descriptive Methods procedure, are as follows:

(A couple

of minor technical points to note here: we have logged and differenced LEADIND

to stationarize it because the RESIDUALS of the ARIMA model are also logged and

differenced--i.e., expressed in units of percentage change. Also, the

Descriptive Methods procedure, like the Forecasting procedure, does not like

variables which begin with too many missing values. Here the missing values at

the beginning of the RESIDUALS variables were replaced by zeroes--typed

in by hand--before running the Descriptive Methods procedure. Actually, the

Forecasting procedure is supposed to automatically draw cross-correlation plots

of the residuals versus other variables, but the graph which is labeled

"Residual Cross-Correlation Plot" merely shows the cross-correlations

of the input variable versus other variables.)

We see that the most significant

cross-correlation is at lag 0, but unfortunately we cannot use that for

forecasting one month ahead. Instead, we must try to exploit the smaller

cross-correlations at lags 1 and/or 2. As a quick test of whether lags of

DIFF(LOG(LEADIND)) are likely to add anything to our ARIMA model, we can use

the Multiple Regression procedure to regress RESIDUALS on lags of

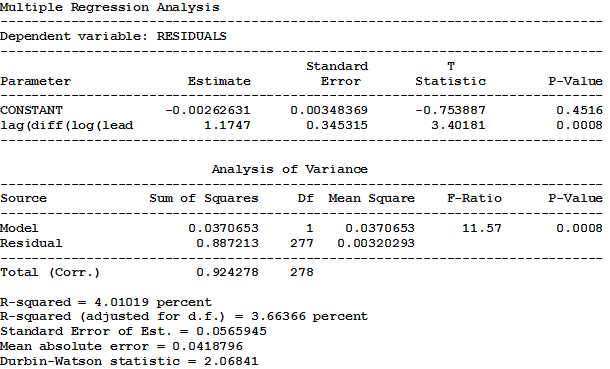

DIFF(LOG(LEADIND)). Here is the result of regressing RESIDUALS on

LAG(DIFF(LOG(LEADIND)),1):

The R-squared value of only 3.66% suggests that not much

improvement is possible. (If two lags of DIFF(LOG(LEADIND)) are used, the

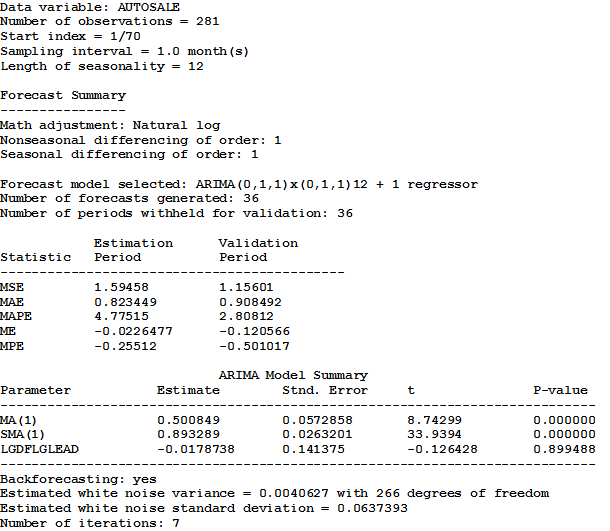

R-squared only increases to 4.06%.) If we return to the ARIMA procedure and add

LAG(DIFF(LOG(LEADIND)),1) as a regressor, we obtain the following model-fitting

results:

(Minor technical point here: we stored the values of

LAG(DIFF(LOG(LEADIND)),1) in a new column, filled in the two missing values at

the beginning with zeroes, and assigned the new column the name LGDFLGLEAD.) We

see that when a coefficient for the lag of DIFF(LOG(LEADIND)) is estimated simultaneously

with the other parameters of the model, it is even less significant than it

was in the regression model for RESIDUALS. The improvement in the

root-mean-squared error is just too small to be noticeable.

The negative result

we obtained here should not be taken to suggest that regressors will never be

helpful in ARIMA models or other time series models. For example, variables

which measure advertising or price levels or the occurrence of promotional

events are often helpful in augmenting ARIMA models (and exponential smoothing

models) for forecasting sales at the level of the firm or product. Remember

that the variable being analyzed here--nationwide sales at automotive

dealers--is a highly aggregated macroeconomic time series. We have learned by

now that the impact on a macroeconomic variable of events which occurred in earlier

periods (e.g., changes in various economic factors that make up the index

of leading indicators) is often most clearly represented in the prior history

of that variable itself. Hence, lagged values of other macroeconomic time

series may have little to add to a forecasting model which has already fully

exploited the history of the original time series. Leading economic indicators

are often more useful when applied as they are intended--namely as indicators

of turning points in business cycles that may have a bearing on the direction

of longer-term trend projections.